Dollar rose broadly overnight, following solid job and services data, and remains firm in Asian session. Nevertheless, the real test lies in today’s non-farm payroll report. As of now, Yen is the second strongest for the week, following the green back. Canadian Dollar is the third strongest, and will face the test of its own job data too. Kiwi and Aussie are the worst performing, together with Sterling.

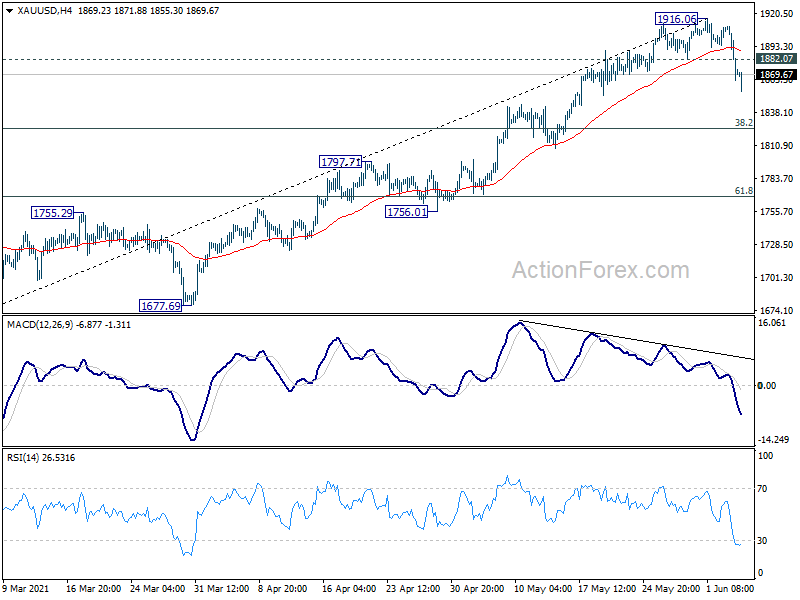

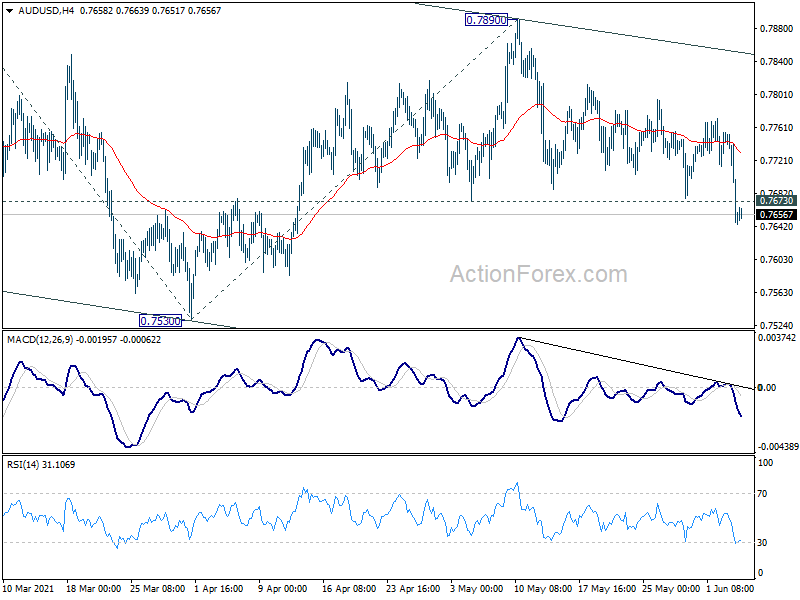

Technically, AUD/USD’s break of 0.7673 support suggests that the pattern from 0.8006 is now in its third leg, targeting 0.7530 support again. To seal the case of near term Dollar reversal, we should ideally see decisive break of 1.4090 support and GBP/USD, as well as 0.9046 resistance in USD/CHF today. Gold’s break of 1882.07 support overnight should confirm short term topping at 1916.06. However, a strong and quick rebound above this support turned resistance could be a warning for the Dollar bulls.

{kind=link}

In Asia, at the time of writing, Nikkei is down -0.41%. Hong Kong HSI is up 0.17%. China Shanghai SSE is up 0.14%. Singapore Strait Times is down -0.15%. Japan 10-year JGB yield is up 0.0014 at 0.088. Overnight, DOW dropped -0.07%. S&P 500 dropped d-0.36%. NASDAQ dropped -1.03%. 10-year yield rose 0.034 to 1.625.

Dollar index rebounded ahead of NFP, eyeing 90.90 resistance

US non-farm payroll employment is once again a major focus today. Markets are expecting 621k job growth in May. Unemployment rate is expected to drop from 6.1% to 5.9%. Average hourly earnings are expected to grow 0.2% mom.

Looking at related data, ADP private jobs grew a massive 978k in the month. More importantly, growth was quite evenly distribution among small, mid, and large companies. Four-week moving average of initial jobless claims dropped sharply from 612k to 428k. However, ISM manufacturing employment dropped notably from 55.1 to 50.9. ISM services employment also dropped from 58.8 to 55.3. There is still room for disappointment considering the relatively high expectations on the NFP numbers.

Dollar staged a strong and broad based rebound overnight. The Dollar index look set to start the third leg of the consolidation pattern from 89.20. Yet, we’d need to see firm break of 90.90 resistance, as well as sustained trading above 55 day EMA to confirm. In that case, stronger rise should follow towards 93.43 resistance in the next few months. However, failure to do so would keep near term outlook bearish for at least another take on 89.20 low.

{kind=link}

Fed Williams: Not is not the time to take any action on tapering

New York Fed President John Williams said, “we’re still quite a ways off from maintaining the substantial further progress we’re really looking for in terms of adjustments to our asset purchase program.” And, “I just don’t think the time is now to take any action.”

“We have to be thinking ahead, planning ahead, so I do think it makes sense for us to be thinking through the various options we may have in the future,” Williams added.

Williams was “very positive” about the economic look. “I expect the economy will adapt to the rapid recovery and we’re going to see very good jobs growth and expect to see really strong GDP growth this year and seeing good growth next year,” he said.

Fed Kaplan: It’s wiser sooner rather than later to discuss tapering

Dallas Fed President Robert Kaplan reiterated that “it would be wiser sooner rather than later to begin discussions about adjusting our purchases with a view to taking the foot off the accelerator gently, gradually, so we can avoid having to depress the brake down the road.”

“At this stage, as it’s clear we are weathering the pandemic and making progress, I don’t think the housing market needs the level of support that the Fed is currently providing,” he added. “I would love to see sooner rather than later a discussion of the efficacy, for example, of those mortgage purchases.”

On the data front

Japan household spending rose 13.0% yoy in April, above expectation of 8.9% yoy. UK PMI construction and Eurozone retail sales will be release in European session. Later in the day, employment data from US and Canada are the major focuses. US will also release factor orders while Canada will release Ivey PMI.

AUD/USD Daily Report

Daily Pivots: (S1) 0.7620; (P) 0.7687; (R1) 0.7728; More…

AUD/USD’s break of 0.7673 support suggests that rebound from 0.7530 has completed at 0.7890 already. More importantly, corrective pattern from 0.8006 high should now be in it’s third leg. Intraday bias is back on the downside for 0.7530 support first. Break there will target 100% projection of 0.8006 to 0.7530 from 0.7890 at 0.7414. We’d expect strong support from there, which coincides with 0.7413 key resistance turned support, to bring reversal.

{kind=link}

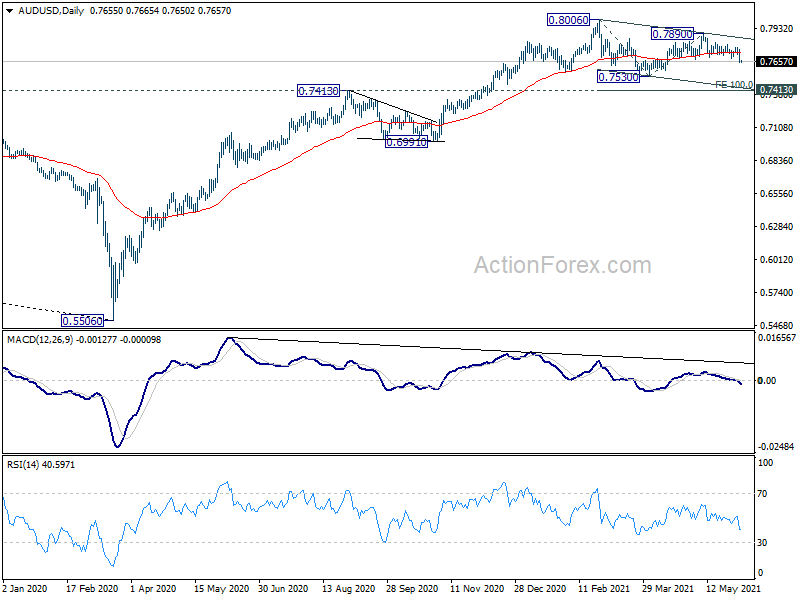

In the bigger picture, whole down trend from 1.1079 (2001 high) should have completed at 0.5506 (2020 low) already. Rise from 0.5506 could either be the start of a long term up trend, or a corrective rise. Reactions to 0.8135 key resistance will reveal which case it is. But in any case, medium term rally is expected to continue as long as 0.7413 resistance turned support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Household Spending Y/Y Apr | 13.00% | 8.90% | 6.20% | |

| 08:30 | GBP | Construction PMI May | 62.3 | 61.6 | ||

| 09:00 | EUR | Eurozone Retail Sales M/M Apr | -0.90% | 2.70% | ||

| 12:30 | CAD | Net Change in Employment May | -20.3K | -207.1K | ||

| 12:30 | CAD | Unemployment Rate May | 8.20% | 8.10% | ||

| 12:30 | CAD | Labor Productivity Q/Q Q1 | -2.00% | |||

| 12:30 | USD | Nonfarm Payrolls May | 621K | 266K | ||

| 12:30 | USD | Unemployment Rate May | 5.90% | 6.10% | ||

| 12:30 | USD | Average Hourly Earnings M/M May | 0.20% | 0.70% | ||

| 14:00 | USD | Factory Orders M/M Apr | 0.40% | 1.10% | ||

| 14:00 | CAD | Ivey Purchasing Managers Index May | 62.3 | 60.6 |