Dollar trades slightly higher in early US session on much better than expected ADP private job data. Though, upside is so far limited, as traders remain cautious ahead of tomorrow’s non-farm payrolls report. Sterling is following as the second strongest for today, then Yen. On the other hand, commodity currencies are generally lower, as led by both Australian and New Zealand Dollars.

Technically, in spite of current recovery, there is no confirmation of a turnaround in Dollar’s bearish outlook. The key near term levels include 1.4090 support in GBP/USD, 0.7673 support in AUD/USD, 0.9046 resistance in USD/CHF and 1.2201 resistance in USD/CAD. Dollar’s selloff could come back any time as long as these levels hold.

In Europe, at the time of writing, FTSE is down -1.11%. DAX is down -0.42%. CAC is down -0.43%. Germany 10-year yield is up 0.0110 at -0.185. Earlier in Asia, Nikkei rose 0.39%. Hong Kong HSI dropped -1.13%. China Shanghai SSE dropped -0.36%. Singapore Strait Times rose 0.13%. Japan 10-year JGB yield rose 0.0076 to 0.087.

US initial jobless claims dropped to 385k, continuing claims ticked up to 3.77m

US initial jobless claims dropped -20k to 385k in the week ending May 29, better than expectation of 410k. Four-week moving average of initial claims dropped -30.5k to 428k. Both figures were lowest since March 14, 2020.

Continuing claims rose 169k to 3771k in the week ending May 22. Four-week moving average of continuing claims rose 23k to 3688k.

US ADP jobs grew 978k, upstick in companies of all sizes

US ADP private sector employment grew 978k in May, well above expectation of 695k. By company size, small businesses added 333k jobs, medium term businesses added 338k, large businesses added 308k. By sector, goods-producing jobs grew 128k, service-providing jobs grew 850k.

“Private payrolls showed a marked improvement from recent months and the strongest gain since the early days of the recovery,” said Nela Richardson, chief economist, ADP. “While goods producers grew at a steady pace, it is service providers that accounted for the lion’s share of the gains, far outpacing the monthly average in the last six months. Companies of all sizes experienced an uptick in job growth, reflecting the improving nature of the pandemic and economy.”

UK PMI services finalized at 62.9, eye-popping growth in Q2

UK PMI Services was finalized at 62.9 in May, up from April’s 62.9, fastest growth in 24 years. PMI Composite was finalized at 62.9, up from April’s 60.7, record high since 1998.

Tim Moore, Economics Director at IHS Markit: “UK service providers reported the strongest rise in activity for nearly a quarter-century during May as the roll back of pandemic restrictions unleashed pent up business and consumer spending. The latest survey results set the scene for an eye-popping rate of UK GDP growth in the second quarter of 2021, led by the reopening of customer-facing parts of the economy after winter lockdowns.”

Eurozone PMI Composite finalized at 57.1, strong growth in Q2, even more impressive in Q3

Eurozone PMI Services was finalized at 55.2 in My, up from April’s 50.0. PMI Composite was finalized at 57.1, up from April’s 53.8. Looking at some member states Ireland PMI Composite rose to record high of 63.5. Spain rose to 174-month high at 59.2. France rose to 10-month high at 57.0. Germany rose to 2-month high at 56.2. Italy rose to 39-month high at 55.7.

Chris Williamson, Chief Business Economist at IHS Markit said: “The eurozone’s vast service sector sprang back into life in May, commencing a solid recovery that looks likely to be sustained throughout the summer… The service sector revival accompanies a booming manufacturing sector, meaning GDP should rise strongly in the second quarter. With a survey record build-up of work-in-hand to be followed by the further loosening of covid restrictions in the coming months, growth is likely to be even more impressive in the third quarter.”

Germany PMI Services was finalized at 52.8 in May, up from April’s 49.9. PMI Composite rose to 56.2, up from April’s 55.8.

France PMI Services was finalized at 56.6 in May, up from April’s 50.3. PMI Composite was finalized at 57.0, up from April’s 51.6.

China Caixin PMI services dropped to 55.1, composite dropped to 53.8

China Caixin PMI Services dropped to 55.1 in May, down from 56.3, below expectation of 56.2. PMI Composite dropped to 53.8, down from 54.7.

Wang Zhe, Senior Economist at Caixin Insight Group said: “To sum up, the expansion in manufacturing and services maintained its momentum as both supply and demand expanded. Overseas demand was generally good, but service exports were affected by the pandemic. The job market continued to improve. In May, services recovered faster than manufacturing. Entrepreneurs were confident about the economic outlook. Inflation remained a crucial concern as the price gauges in manufacturing and services both rose last month.

Australia trade surplus rose to AUD 8B

Australia goods and services exports rose 3% mom to AUD 39.8B in April. Imports dropped -3% to AUD 31.7B. Trade surplus rose from AUD 2.2B to AUD 8.0B, matched expectations. Retail sales rose 1.1% mom, unchanged from preliminary results.

AiG Performance of Construction Index dropped -0.8 pts to 58.3, “largely maintaining the strong pace of post-2020 recovery following on from a record high in March“.

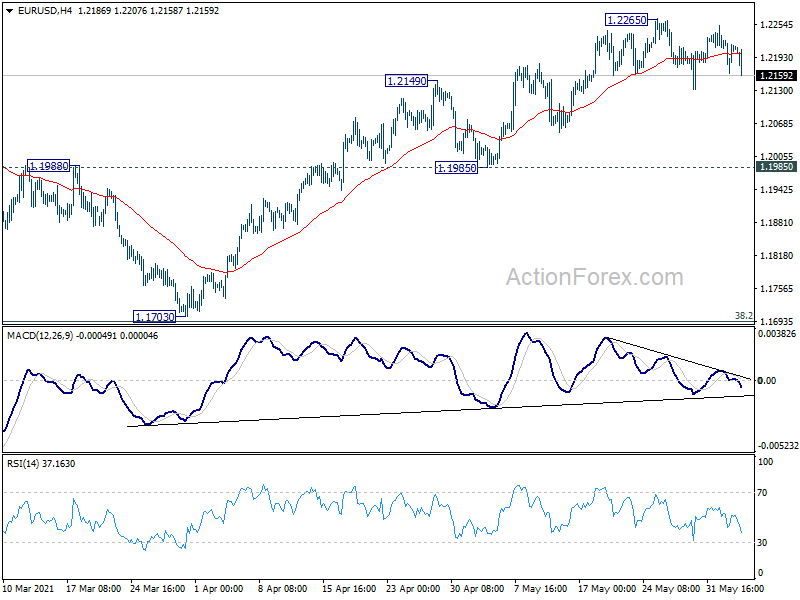

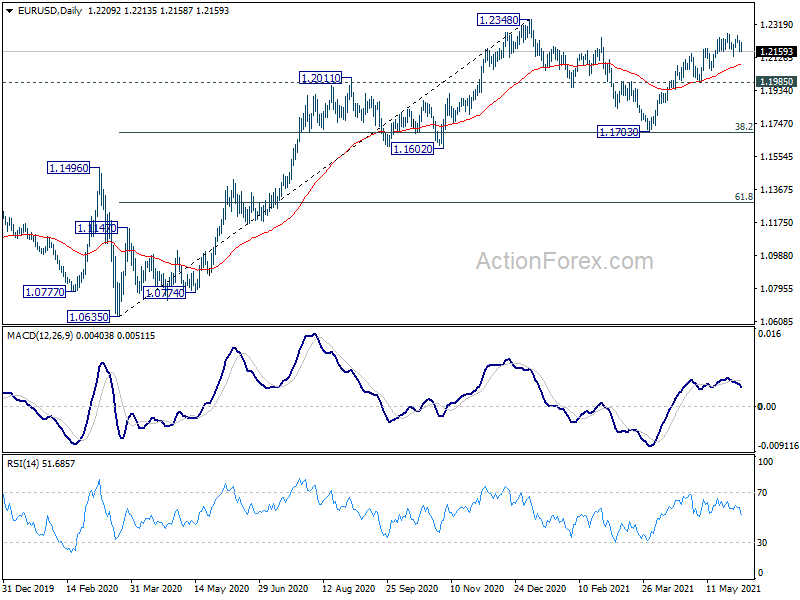

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2174; (P) 1.2200; (R1) 1.2237; More…

EUR/USD drops mildly today but intraday bias remains neutral first. On the upside, above 1.2265 will resume the rise from 1.1703 to retest 1.2348 high. On the downside, firm break of 1.1985 support should confirm that consolidation pattern from 1.2348 has started the third leg. Deeper fall would then be seen back to 1.1703 support.

{kind=link}

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1602 support holds. Reaction from 1.2555 should reveal underlying long term momentum in the pair.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Construction May | 58.3 | 59.1 | ||

| 01:30 | AUD | Retail Sales M/M Apr | 1.10% | 1.10% | 1.10% | |

| 01:30 | AUD | Trade Balance (AUD) Apr | 8.03B | 8.00B | 5.57B | |

| 01:45 | CNY | Caixin Services PMI May | 55.1 | 56.2 | 56.3 | |

| 07:45 | EUR | Italy Services PMI May | 53.1 | 52 | 47.3 | |

| 07:50 | EUR | France Services PMI May F | 56.6 | 56.6 | 56.6 | |

| 07:55 | EUR | Germany Services PMI May F | 52.8 | 52.8 | 52.8 | |

| 08:00 | EUR | Eurozone Services PMI May F | 55.2 | 55.1 | 55.1 | |

| 08:30 | GBP | Services PMI May F | 62.9 | 61.8 | 61.8 | |

| 11:30 | USD | Challenger Job Cuts Y/Y May | -93.80% | -96.60% | ||

| 12:15 | USD | ADP Employment Change May | 978K | 695K | 742K | 654K |

| 12:30 | USD | Initial Jobless Claims (May 28) | 385K | 410K | 406K | 405K |

| 12:30 | USD | Nonfarm Productivity Q1 | 5.40% | 5.50% | 5.40% | |

| 12:30 | USD | Unit Labor Costs Q1 | 1.70% | -0.40% | -0.30% | |

| 13:45 | USD | Services PMI May F | 70.1 | 70.1 | ||

| 14:00 | USD | ISM Services PMI May | 62.9 | 62.7 | ||

| 14:00 | USD | ISM Services Employment May | 58.8 | |||

| 14:30 | USD | Natural Gas Storage | 95B | 115B | ||

| 15:00 | USD | Crude Oil Inventories | -1.0M | -1.7M |