Dollar recovered overnight, with help from mild risk aversion and some slight hawkish twists in FOMC minutes. Yet, it couldn’t manage to break through any near term technical level yet. Euro remains the strongest one for the week at this point, followed by Yen. Commodity currencies are the generally weaker ones while Aussie is getting no special support from weaker than expected job data. Canadian Dollar was also dragged down by the decline in oil prices.

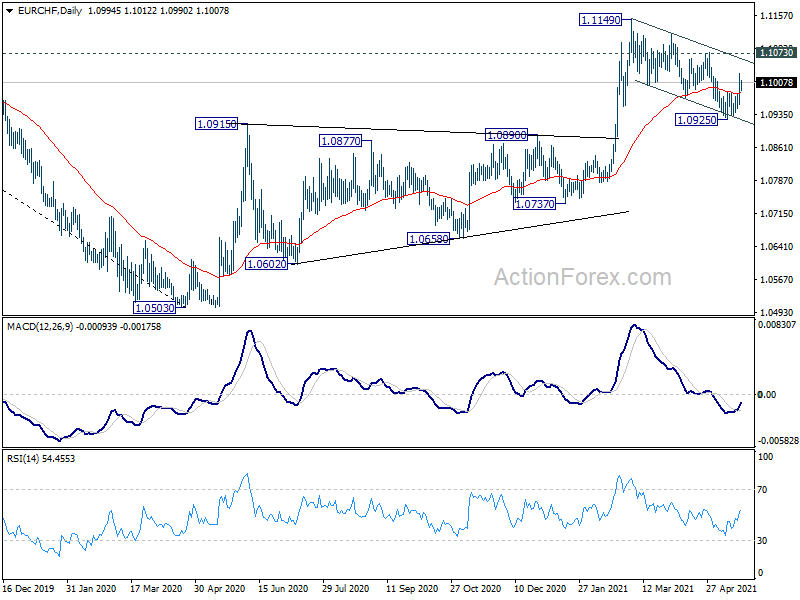

Technically, the fall in Swiss Franc is worth a note, following the rally in German yield this week. EUR/CHF rebounded notably ahead of 1.0915 key resistance turned support. Break of 1.1073 resistance ahead would indicate completion of the correction from 1.1149 and bring resumption of up trend from 1.0503.

{kind=link}

In Asia, at the time of writing, Nikkei is up 0.01%. Hong Kong HSI is down -0.69%. China Shanghai SSE is down -0.29%. Singapore Strait Times is up 0.28%. Japan 10-year JGB yield is up 0.004 at 0.079. Overnight, DOW dropped -0.48%. S&P 500 dropped -0.29%. NASDAQ dropped -0.03%. 10-year yield rose 0.042 to 1.683.

Fed minutes: Some think it might be appropriate to discuss tapering in upcoming meetings

The main hawkish surprise from the FOMC minutes released overnight was that, “a number of participants suggested that if the economy continued to make rapid progress toward the Committee’s goals, it might be appropriate at some point in upcoming meetings to begin discussing a plan for adjusting the pace of asset purchases.”

Also, “a couple of participants commented on the risks of inflation pressures building up to unwelcome levels before they become sufficiently evident to induce a policy reaction.” Some participants mentioned “upside risks around the inflation outlook that could arise if temporary factors influencing inflation turned out to be more persistent than expected.”

But overall, “after the transitory effects of these factors fade, participants generally expected measured inflation to ease. Looking further ahead, participants expected inflation to be at levels consistent with achieving the Committee’s objectives over time.”

Australia employment dropped -30.6k, but not clear JobKeeper impact

Australia employment dropped -30.6k in April worse than expectation of 15k rise. Full-time jobs rose 33.8k while part-time jobs dropped -64.4k. Total employment was 45.9k, or 0.4%, higher than March 2020 level. But unemployment rate dropped to 5.5%, down from 5.7%, better than expectation of 5.5%. Participation rate dropped -0.3% to 66.0%.

“We have not seen large changes in the indicators that would suggest a clear JobKeeper impact, such as an increase in people working reduced or zero hours for economic reasons or because they were leaving their job. We also haven’t seen large net flows out of employment across many population groups,” Bjorn Jarvis, head of labour statistics at the ABS said.

Also from Australia, consumer inflation expectations rose to 3.5% in May, up from 3.2%.

Japan exports jumped 38% yoy in Apr, fastest in more than a decade

Japan’s exports rose 38.0% yoy to JPY 7181B in April. That’s the fastest growth in more than a decade since 2010, as led by US bound shipments of cars and parts. Also, Chinese demand for chip-making equipment was also a boost. Exports to China jumped 33.9% yoy while exports to the US rose 45.1% yoy. Imports rose 12.8% yoy to 6925B. Trade surplus came in at JPY 255B.

In seasonally adjusted terms, exports rose 2.5% mom to JPY 6856B. Imports rose 7.5% mom to JPY 6791B. Trade surplus narrowed to JPY 65B.

Also from Japan, machine orders rose 3.7% mom in March, below expectations of 6.4% mom.

Looking ahead

Germany PPI and Eurozone current account will be featured in European session. Canada new housing price index, US jobless claim and Philly Fed survey will be released later in the day.

AUD/USD Daily Report

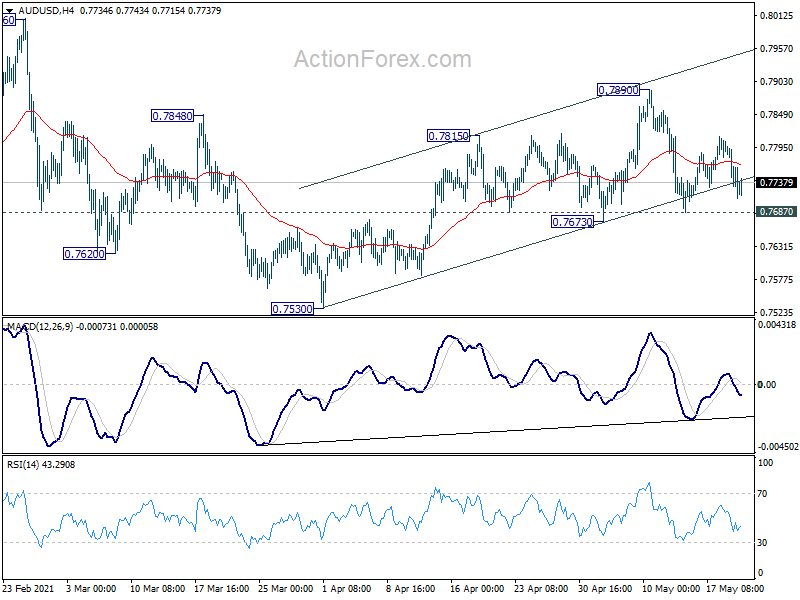

Daily Pivots: (S1) 0.7691; (P) 0.7746; (R1) 0.7782; More…

AUD/USD is staying in range above 0.7687 support and intraday bias remains neutral first. Another rise is mildly in favor. Break of 0.7890 will target a test on 0.8005 high. However, firm break of 0.7687 support should extend the correction from 0.8006 with another falling leg. Intraday bias will be turned back to the downside for 0.7530 support and possibly below.

{kind=link}

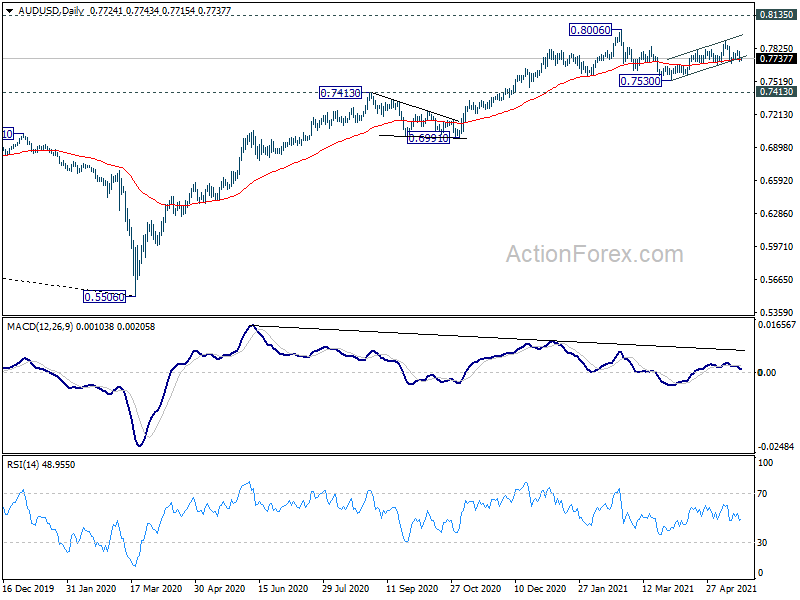

In the bigger picture, whole down trend from 1.1079 (2001 high) should have completed at 0.5506 (2020 low) already. Rise from 0.5506 could either be the start of a long term up trend, or a corrective rise. Reactions to 0.8135 key resistance will reveal which case it is. But in any case, medium term rally is expected to continue as long as 0.7413 resistance turned support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Apr | 0.07T | 0.07T | 0.30T | 0.37T |

| 23:50 | JPY | Machinery Orders M/M Mar | 3.70% | 6.40% | -8.50% | |

| 01:00 | AUD | Consumer Inflation Expectations May | 3.50% | 3.60% | 3.20% | |

| 01:30 | AUD | Employment Change Apr | -30.6K | 15.0K | 70.7K | 77.0K |

| 01:30 | AUD | Unemployment Rate Apr | 5.50% | 5.60% | 5.60% | 5.70% |

| 06:00 | EUR | Germany PPI M/M Apr | 1.00% | 0.90% | ||

| 06:00 | EUR | Germany PPI Y/Y Apr | 4.50% | 3.70% | ||

| 08:00 | EUR | Eurozone Current Account (EUR) Mar | 24.3B | 25.9B | ||

| 12:30 | CAD | ADP Employment Change Apr | 634.8K | |||

| 12:30 | CAD | New Housing Price Index M/M Apr | 1.40% | 1.10% | ||

| 12:30 | USD | Initial Jobless Claims (May 14) | 450K | 473K | ||

| 12:30 | USD | Philadelphia Fed Manufacturing May | 40.8 | 50.2 | ||

| 14:30 | USD | Natural Gas Storage | 60B | 71B |