Dollar’s decline slowed in Asian session today, but remains generally weak, in particular against European majors. Though, indecisive risk sentiment is somehow limiting upside in commodity currencies, with Canadian Dollar following oil prices lower today. There is prospect of more volatility in the markets today, with consumer inflation data from UK and Canada featured. FOMC minutes will also catch some attention.

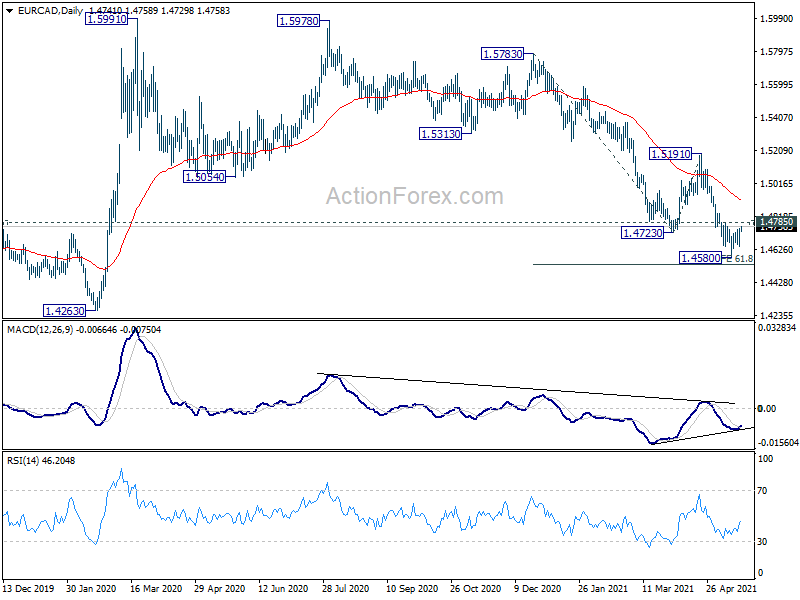

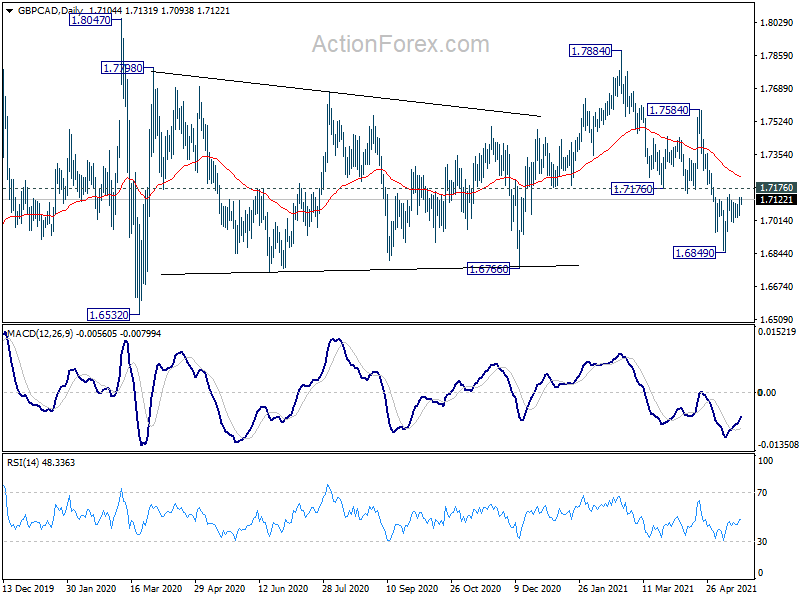

Technically, Canadian crosses could be worth a note today as the Loonie has lost much upside momentum recently. EUR/CAD recovered after hitting 1.4580. Break of 1.4785 resistance will suggest short term bottoming and bring stronger rebound back to 55 day EMA at 1.4917. GBP/CAD is also eyeing 1.7176 support turned resistance and firm break there should confirm short term bottoming too. Nevertheless, the developments could very much depend on the Canadian inflation data, and the reactions today.

{kind=link}

{kind=link}

In Asia, at the time of writing, Nikkei is down -1.40%. Hong Kong is on holiday. China Shanghai SSE is down -0.33%. Singapore Strait Times is down -0.46%. Japan 10-year JGB yield is down -0.0043 at 0.076. Overnight, DOW dropped -0.78%. S&P 500 dropped -0.85%. NASDAQ dropped -0.56%. 10-year yield rose 0.002 to 1.642.

Australia consumer sentiment dropped -4.8%, still second highest since 2010

Australia Westpac-Melbourne Institute consumer sentiment dropped -4.8% mom to 113.1 in May, down from 118.8. Still, it’s the second highest print for the index since April 2010. Westpac said, “The fall may also represent some disappointment in the Federal Budget as a very generous Budget was still unable to exceed the exuberant expectations of the community.”

On RBA policy, Westpac expects the board to extend QE to a further AUD 100B starting in September, and to switch the target bond in the yield curve control from April 2024 to November 2024. It said, “this view is based on the expectation that the Board will be committed to monetary stimulus (reducing QE or restricting YCC to the April bond are akin to tightening policy) for the remainder of 2021.”

Also released, wage price index rose 0.6% qoq in Q1, above expectation of 0.5% qoq.

New Zealand PPI input jumped 2.1% qoq, output rose 1.2% qoq, electricity price surged

New Zealand PPI input jumped 2.1% qoq in Q1, versus expectation of 0.0% qoq. PPI output rose 1.2% qoq, above expectation of 0.0% qoq. The largest output industry contributions were from electricity and gas supply, which was up 17.4%. Petroleum and coal product manufacturing rose 12.2%. daily cattle farming rose 5.1%.

The largest input industry contributions were from electricity and gas supply, which was up 28.7%. Dairy production manufacturing rose 4.7%. Petroleum and coal product manufacturing rose 9.3%.

“Lower lake levels in the South Island have driven up wholesale prices for electricity generation, while an unexpected fall in production at the Pohokura gas field has seen gas supply prices also increase,” business prices delivery manager Bryan Downes said. “The quarterly price change is the largest since 2018 but is nowhere near the magnitude seen in the 2008 power crisis.”

US, Canada and Mexico commit to prohibit import of forced labor produced goods

Trade ministers from the US, Canada and Mexico held “robust” talks on the new U.S.-Mexico-Canada trade agreement, which took effect last July. In a joint statement, they said, “the USMCA commits us to a robust and inclusive North American economy that serves as a model globally for competitiveness, while prioritizing the interests of workers and underserved communities.”

Additionally, the statement noted, “the United States, Mexico, and Canada discussed our shared obligation to ensure the Agreement’s prohibition of the importation of goods produced by forced labor and recommitted to working closely to promote a fair, rules-based international trading system where products made with forced labor do not enter the trading system.”

Dollar index broke 90 as focus turns to FOMC minutes

Dollar’s selloff continued overnight as focus now turns to minutes of April 27-28 FOMC meeting. While markets were a bit nervous on much stronger than expected consumer inflation readings, Fed officials were in unison in toning down the threat. Current jump in price is generally viewed as transitory by the policymakers. On the other hand, recent data like non-farm payrolls and retail sales argue that the recovery might be more vulnerable than it looks. The minutes would reiterate that Fed is still far from even considering tapering nor interest rate normalization.

Dollar index resumed the fall from 93.43 this week and breaks 90 handle. It’s on track to retest 89.20 low. At this point, it’s rather unsure if such decline is the second leg of the consolidation pattern from 89.20, or it’s resuming the down trend from 102.99. We’ll stay cautious on a strong rebound from 89.20 level. Break of 90.90 resistance will suggest that the near term trend has changed and stronger rebound would be seen back towards 93.43 resistance. Though, firm break of 89.20 will, of course, confirm down trend resumption. In that case, we should see EUR/USD taking out 1.2348 resistance in tandem.

{kind=link}

Looking ahead

UK inflation data, CPI, RPI and PPI will be the main focus in European session. Eurozone will release April CPI final. Later in the day, Canada will release CPI too.

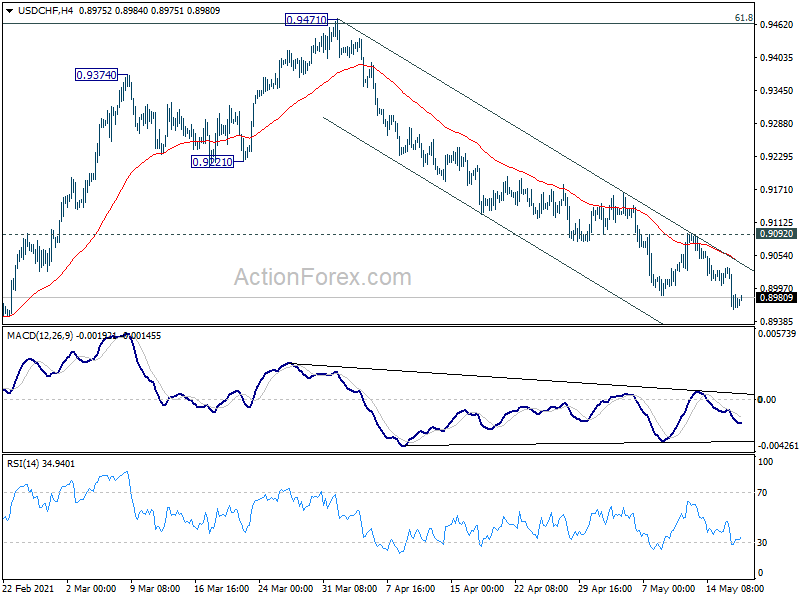

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8947; (P) 0.8991; (R1) 0.9021; More….

Intraday bias in USD/CHF remains on the downside at this point. Current fall from 0.9471 should target a test on 0.8756 low. On the upside, break of 0.9092 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

{kind=link}

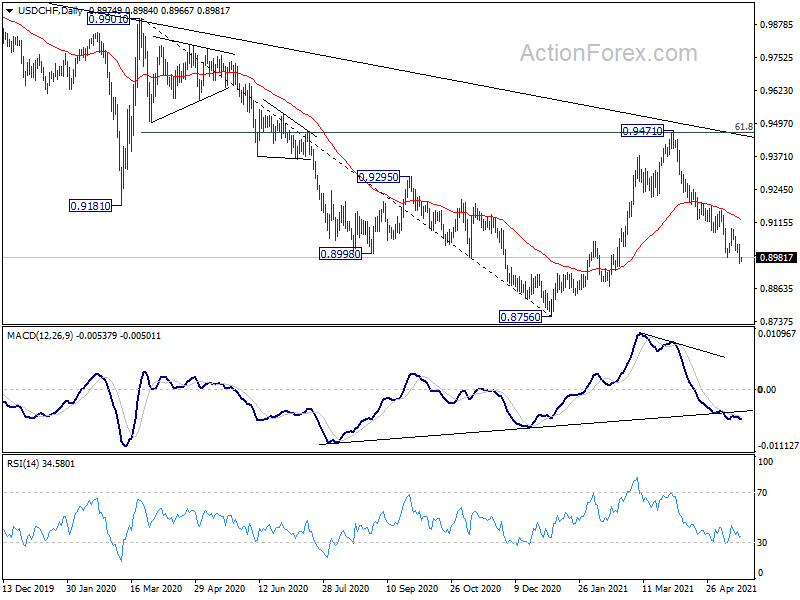

In the bigger picture, rejection by 61.8% retracement of 0.9901 to 0.8756 at 0.9464 argues that rebound from 0.8756 was probably just a corrective move. That is, larger down trend from 1.0237 might be still in progress. Medium term bearish is also affirmed as the pair is now far below falling 55 week EMA. Firm break of 0.8756 low will target 61.8% projection of 1.0237 to 0.8756 from 0.9471 at 0.8556 next.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | PPI Input Q/Q Q1 | 2.10% | 0.00% | 0.00% | 0.10% |

| 22:45 | NZD | PPI Output Q/Q Q1 | 1.20% | 0.00% | 0.40% | 0.50% |

| 00:30 | AUD | Westpac Consumer Confidence May | -4.80% | 6.20% | ||

| 01:30 | AUD | Wage Price Index Q/Q Q1 | 0.60% | 0.50% | 0.60% | |

| 04:30 | JPY | Industrial Production M/M Mar F | 2.20% | 2.20% | ||

| 06:00 | GBP | CPI M/M Apr | 0.50% | 0.30% | ||

| 06:00 | GBP | CPI Y/Y Apr | 1.40% | 0.70% | ||

| 06:00 | GBP | Core CPI Y/Y Apr | 1.20% | 1.10% | ||

| 06:00 | GBP | RPI M/M Apr | 0.80% | 0.30% | ||

| 06:00 | GBP | RPI Y/Y Apr | 2.30% | 1.50% | ||

| 06:00 | GBP | PPI Input M/M Apr | 0.60% | 1.30% | ||

| 06:00 | GBP | PPI Input Y/Y Apr | 4.40% | 5.90% | ||

| 06:00 | GBP | PPI Output M/M Apr | 0.40% | 0.50% | ||

| 06:00 | GBP | PPI Output Y/Y Apr | 3.50% | 1.90% | ||

| 06:00 | GBP | PPI Core Output M/M Apr | 0.30% | 0.40% | ||

| 06:00 | GBP | PPI Core Output Y/Y Apr | 1.80% | 1.70% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Apr F | 1.60% | 1.60% | ||

| 09:00 | EUR | Eurozone CPI – Core Y/Y Apr F | 0.80% | 0.80% | ||

| 12:30 | CAD | CPI M/M Apr | 0.20% | 0.50% | ||

| 12:30 | CAD | CPI Y/Y Apr | 3.20% | 2.20% | ||

| 12:30 | CAD | CPI Common Y/Y Apr | 1.70% | 1.50% | ||

| 12:30 | CAD | CPI Median Y/Y Apr | 2.10% | 2.10% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Apr | 2.20% | 2.20% | ||

| 14:30 | USD | Crude Oil Inventories | 1.5M | -0.4M | ||

| 18:00 | USD | FOMC Minutes |