Dollar retreats mildly in early US session after weaker than expected job data. Also, treasury yield is retreating mildly while stocks point to higher open, in particular NASDAQ. Pre-holiday trading in the currency markets is generally mixed. Aussie tumbled earlier today but has recovered a large part of the losses quickly. Sterling is trying hard to extend this week’s rise against Euro and Yen, but struggles to accomplish it yet.

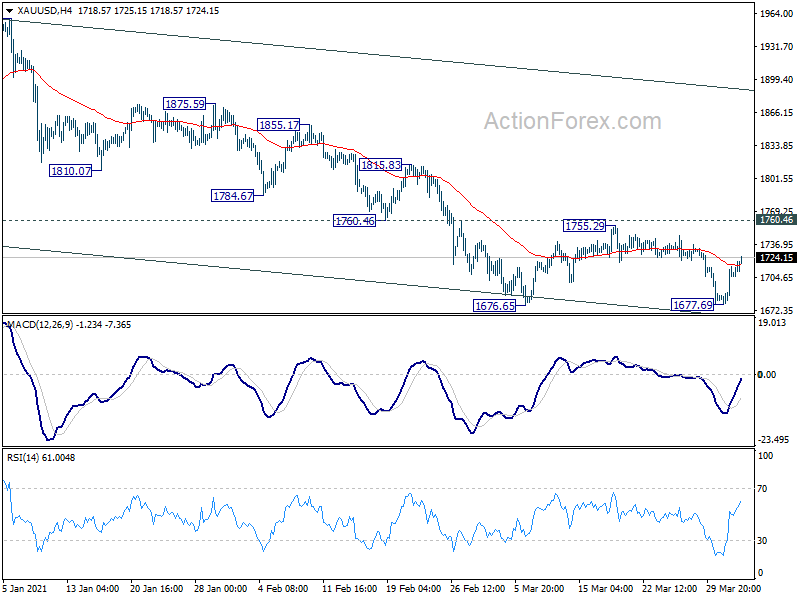

Technically, Gold defended 1676.65 support in the first attempt this week and recovered. Still, it’s just started the third leg of the consolidation pattern from 1676.65. Outlook will stay bearish as long as 1760.46 resistance holds, and downside breakout is still in favor. The development could correspond to some consolidations in Dollar, before extending recent rises, probably late next week.

{kind=link}

In Europe, currently FTSE is up 0.54%. DAX is up 0.50%. CAC is up 0.44%. Germany 10-year yield is down -0.0318 at -0.322. Earlier in Asia, Nikkei rose 0.72%. Hong Kong HSI rose 1.97%. China Shanghai SSE rose 0.71%. Singapore Strait Times rose 0.52%. Japan 10-year JGB yield closed flat at 0.116.

US initial jobless claims rose to 719k, continuing claims at 3.8m

US initial jobless claims rose 61k to 719k in the week ending March 27, above expectation of 678k. Four-week moving average of initial claims dropped -10.5k to 719k.

Continuing claims dropped -46k to 3794k in the week ending March 20. Four-week moving average of continuing claims dropped -147k to 3979k.

ECB Lane: 2021 rise in inflation just the unwinding of 2020 disinflationary forces

ECB chief economist Philip Lane said in a blog post that “the volatility of inflation during 2020-2021 can be largely attributed to the nature of the pandemic shock”. Increase in inflation in 2021 can be ” best interpreted as the unwinding of disinflationary forces that took hold in 2020″ only.

Medium term inflation outlook “remains subdued, amid “weak demand and substantial slack in labour and product market”. Against this background, Lane said, “ensuring favourable financing conditions is fundamental to restoring inflation momentum and guiding the formation of inflation expectations”

“Offsetting the negative pandemic shock to the inflation outlook is only the first stage of the monetary policy challenge,” he added. Even after the disinflationary pressures are offset, ” we will have to ensure that the monetary policy stance delivers the timely and robust convergence to our inflation aim.”.

Eurozone PMI manufacturing finalized at 62.5 in Mar, improvement broad based across the region

Eurozone PMI Manufacturing was finalized at 62.5 in March, up from February’s 57.9. Manufacturing economy “performed extremely strongly”, with “operating conditions improving to the greatest degree in nearly 24 years of data collection.”

Looking at some member states, Germany PMI manufacturing rose to 66.6, a record high. The Netherlands rose to 64.7, record high. Australia rose to 63.4, 39-month high. Italy rose to 59.8, 252-month high. France rose to 59.3, 246-month high. Ireland rose to 57.1, 8-month high. Spain rose to 56.9, 171-month high. Even Greece rose to 51.8, 13-month high.

Chris Williamson, Chief Business Economist at IHS Markit said: “Although centred on Germany… the improving trend is broad based across the region as factories benefit from rising domestic demand and resurgent export growth…. Driving the upturn has been a marked improvement in business confidence in recent months, with expectations of growth in the year ahead running at record highs in February and March.”

UK PMI manufacturing finalized at 58.9 in Mar, signs of spring appeared

UK PMI Manufacturing was finalized at 58.9 in March, up from February’s 55.1. That’s the highest level in 121 months since February 2011. Business optimism rose to seven-year high. But supply-chain disruption and inflationary pressures built.

Rob Dobson, Director at IHS Markit: “Signs of Spring have appeared in the UK manufacturing sector, with the PMI hitting its highest level in a decade… Weak export sales and supply-chain issues are likely to remain constraints on growth moving forward, however… Demand outstripping supply to such a wide extent is meanwhile driving up prices… The longer these inflationary and supply-chain worries persist, the greater the potential to curb the strength of the upturn as the economy unlocks in the coming weeks and months.”

Japan Tankan large manufacturing index rose to 5 in Q1, highest since Q3 2019

Japan Tankan Large Manufacturing Index rose to 5 in Q1, up from -10, above expectation of 0. That’s also the highest level since Q3 2019. Non-Manufacturing Index rose to -1, up from -5, above expectation of -5. Large Manufacturing Outlook rose to 4, up from -8, matched expectations. Non-Manufacturing Outlook rose to -1, up from -6, above expectation of -2. All industry Capex rose 3.0%, above expectation of 1.4%.

Also released, PMI Manufacturing was finalized at 52.7 in March, up from February’s 51.4. Usamah Bhatti, Economist at IHS Markit, said: “The Japanese manufacturing sector continued to gather some positive momentum at the end of the first quarter of 2021… Beyond the immediate future, Japanese manufacturers were confident that output would continue to rise over the coming 12 months… Currently, IHS Markit estimates that industrial production in Japan will grow 7.7% in 2021, yet this does not fully recover the output lost in 2020.”

China Caixin PMI manufacturing dropped to 50.6, growing inflationary pressure

China Caixin Manufacturing PMI dropped to 50.6 in March, down from 50.9, missed expectation of 51.0. Markit noted that production increased again amid further uptick in sales. Export orders rose for the first time in three months. Inflationary pressures also picked up.

Australia AiG manufacturing rose to 59.9 in Mar, highest since 2018

Australia AiG Performance of Manufacturing Index rose to 59.9 in March, up from 58.8. That’s the highest level since March 2018, and indicates a sixth consecutive month of strong recovery. Looking at some details, production dropped -8.6 to 57.2. Employment rose 8.2 to 66.0. New orders rose 3.6 to 63.5. Exports dropped -2.8 to 51.3. Input prices dropped -2.8 to 71.3. Selling prices rose 8.5 to 59.7.

Australia exports dropped -1% mom in Feb, imports rose 5%

Australia goods and services exports dropped -1% mom to AUD 38.93B in February. Goods and services imports rose 5% mom to AUD 31.40B. Trade surplus came in at AUD 7.53B, down form January’s AUD 9.62B, below expectation of AUD 9.40B.

Retail sales dropped -0.8% mom in February, revised up from preliminary reading of -1.1% mom.

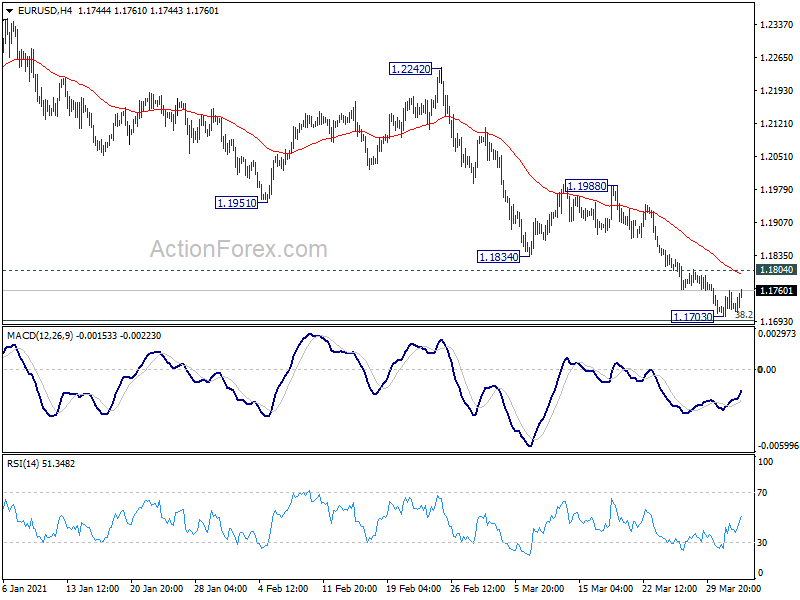

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1703; (P) 1.1731; (R1) 1.1759; More….

Intraday bias in EUR/USD is turned neutral with a temporary low firmed at 1.1703, just ahead of 38.2% retracement of 1.0635 to 1.2348 at 1.1694. In case of another fall, we’d expect strong support from 1.1602 to contain downside to complete the whole correction from 1.2348. On the upside, above 1.1804 minor resistance will turn bias back to the upside for rebound to 1.1988 resistance.

{kind=link}

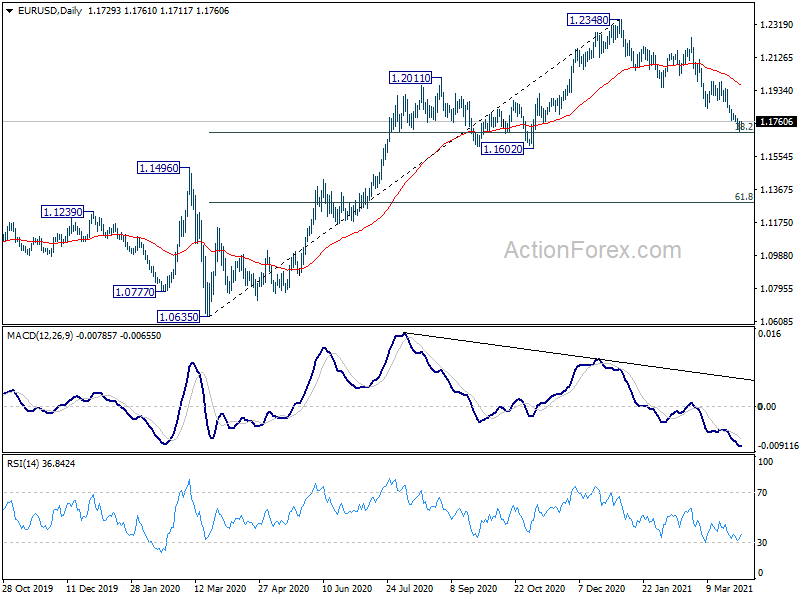

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1602 support holds. However, sustained break of 1.1602 will argue that whole rise from 1.10635 has completed. Deeper fall would be seen to 61.8% retracement of 1.0635 to 1.2348 at 1.1694 at 1.1289.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Mfg Index Mar | 59.9 | 58.8 | ||

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q1 | 4 | 4 | -8 | |

| 23:50 | JPY | Tankan Non – Manufacturing Outlook Q1 | -1 | -2 | -6 | |

| 23:50 | JPY | Tankan Large Manufacturing Index Q1 | 5 | 0 | -10 | |

| 23:50 | JPY | Tankan Non – Manufacturing Index Q1 | -1 | -5 | -5 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q1 | 3.00% | 1.40% | -1.20% | |

| 00:30 | JPY | Jibun Bank Manufacturing PMI Mar F | 52.7 | 52 | 52 | |

| 00:30 | AUD | Retail Sales M/M Feb | -0.80% | -1.10% | -1.10% | 0.30% |

| 00:30 | AUD | Trade Balance(AUD) Feb | 7.53B | 9.40B | 10.14B | 9.62B |

| 01:45 | CNY | Caixin Manufacturing PMI Mar | 50.6 | 51 | 50.9 | |

| 06:00 | EUR | Germany Retail Sales M/M Feb | 1.20% | 2.00% | -4.50% | |

| 06:30 | CHF | Real Retail Sales Y/Y Feb | -6.30% | -0.50% | -0.70% | |

| 06:30 | CHF | CPI M/M Mar | 0.30% | 0.40% | 0.20% | |

| 06:30 | CHF | CPI Y/Y Mar | -0.20% | -0.30% | -0.50% | |

| 07:45 | EUR | Italy Manufacturing PMI Mar | 59.8 | 59.7 | 56.9 | |

| 07:50 | EUR | France Manufacturing PMI Mar F | 59.3 | 58.6 | 58.8 | |

| 07:55 | EUR | Germany Manufacturing PMI Mar F | 66.6 | 66.6 | 66.6 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Mar F | 62.5 | 62.4 | 62.4 | |

| 08:30 | GBP | Manufacturing PMI Mar F | 58.9 | 57.9 | 57.9 | |

| 11:30 | USD | Challenger Job Cuts Y/Y Mar | -86.20% | -39.10% | ||

| 12:30 | CAD | Building Permits M/M Feb | 2.10% | -1.50% | 8.20% | 6.90% |

| 12:30 | USD | Initial Jobless Claims (Mar 26) | 719K | 678K | 684K | 658K |

| 13:30 | CAD | Manufacturing PMI Mar | 54.8 | |||

| 13:45 | USD | Manufacturing PMI Mar | 59.2 | 59 | ||

| 14:00 | USD | ISM Manufacturing PMI Mar | 61 | 60.8 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Mar | 80 | 86 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Mar | 53 | 54.4 | ||

| 14:00 | USD | Construction Spending M/M Feb | -1.00% | 1.70% | ||

| 14:30 | USD | Natural Gas Storage | -20B | -36B |