Australian Dollar remains the strongest one for today, maintaining most of post-CPI gains. But Yen is catching up with broad based recovery. Euro softens despite improvement in German business climate, and Sterling is trading lower too, while Kiwi stays as the worst. Dollar and Canadian are mixed awaiting BoC rate decision.

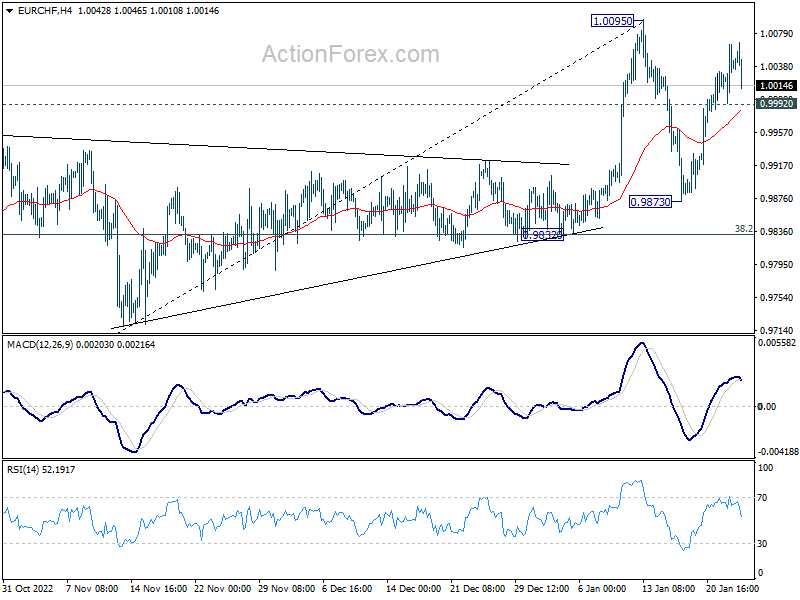

Technically, EUR/CHF is worth a watch in the upcoming session. Up trend resumption through 1.0095 is not envisaged in the first attempt. Indeed, break of 0.9992 minor support will argue that corrective pattern from 1.0095 is already starting the third leg. Deeper decline would then be seen back towards 0.9873 support. If happens, that might be accompanied by weakness in Euro elsewhere, in particular a deeper pull back in EUR/USD.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.11%. DAX is down -0.39%. CAC is down -0.32%. Germany 10-year yield is down -0.073 at 2.082. Earlier in Asia, Nikkei rose 0.35%. Japan 10-year JGB yield rose 0.0319 to 0.444. Singapore Strait Times rose 1.79%. Hong Kong and China were still on holiday.

Germany Ifo business climate rose to 90.2, starting new year with more confidence

Germany Ifo Business Climate rose slightly from 88.6 to 90.2 in January, below expectation of 90.5. Current Assessment ticked down from 94.4 to 94.1, below expectation of 95.0. Expectations index, on the other hand, improved from 83.2 to 86.4, above expectation of 85.0.

By sector, manufacturing rose from -5.7 to -0.7. Services rose from -1.2 to 0.2. Trade rose from -20.0 to -15.4. Construction also rose slightly from -21.9 to -21.6.

Ifo said: “Sentiment in the German economy has brightened. The ifo Business Climate Index rose to 90.2 points in January, up from 88.6 points in December. This is due to considerably less pessimistic expectations. Companies were, however, somewhat less satisfied with their current situation. The German economy is starting the new year with more confidence.”

Japan government downgrades economic assessment

Japan Cabinet Office lowers its monthly economic assessment for the first in 11 months. It said, “the economy is recovering moderately but some weakness is seen recently.”

Also assessment on exports was downgraded for the first time since 2011. Both exports and imports are “weakening recently” compared with its previous view of “almost flat” last month.

“China’s coronavirus rebound could affect Japan’s exports and production and such a possibility has become clearer than last month,” said an official at the Cabinet Office.

Assessment on domestic demand and private consumption was maintained as “picking up moderately”.

New Zealand CPI unchanged at 7.2% yoy in Q4

New Zealand CPI rose 1.4% qoq in Q4, slightly below expectation of 1.5% qoq. Annual CPI was unchanged at 7.2% yoy, above expectation of 7.1% yoy, comparing to the peak at 7.3% yoy in Q2.

StatsNZ said, “Housing and household utilities was the largest contributor to the December 2022 annual inflation rate. This was due to rising prices for both constructing and renting housing.”

The quarterly rise in inflation was “influenced by rising prices in the housing and household utilities, food, and recreation and culture groups.”

Australia CPI rose to 8.4% yoy in Dec, 7.8% yoy in Q4

Australia CPI rose 1.9% qoq in Q4, above expectation of 1.7% qoq. Annual CPI accelerated from 7.3% yoy to 7.8% yoy, above expectation of 7.5% yoy. RBA trimmed mean CPI also accelerated from 6.1% yoy to 6.9% yoy, above expectation of 6.5% yoy.

Michelle Marquardt, ABS head of prices statistics, said “This is the fourth consecutive quarter to show a rise greater than any seen since the introduction of the Goods and Services Tax (GST) in 2000. The increase for the quarter was slightly higher than the quarterly movements for the September and June quarters last year (both 1.8 per cent).”

“The annual increase for the CPI is the highest since 1990. Annual inflation for goods such as new dwellings and automotive fuel steadied this quarter, however we saw an uptick in inflation for services such as holidays and restaurant meals,” Marquardt said.

Monthly CPI accelerated from 7.3% yoy to 8.4% yoy in December, well above expectation of 7.7% yoy.

Marquardt said, “The monthly indicator recorded the largest annual rise in the series in December. The most significant contributors in the 12 months to December were New dwellings, up 16.0 per cent, and Holiday travel and accommodation, up 29.3 per cent. Airfare and accommodation prices rose in response to strong demand over the Christmas holiday period.”

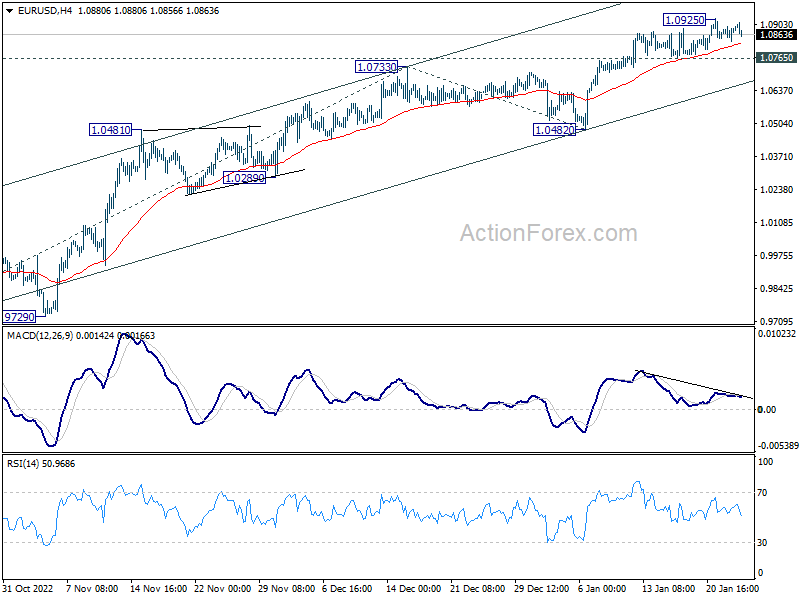

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0850; (P) 1.0874; (R1) 1.0913; More…

Intraday bias in EUR/USD is turned neutral first but further rally is expected with 1.0765 support intact. Break of 1.0925 will resume the rally from 0.9534 to 61.8% projection of 0.9630 to 1.0733 from 1.0482 at 1.1164 next. On the downside, though, break of 1.0765 support should now indicate short term topping, and turn bias back to the downside for 55 day EMA (now at 1.0557).

{kind=link}

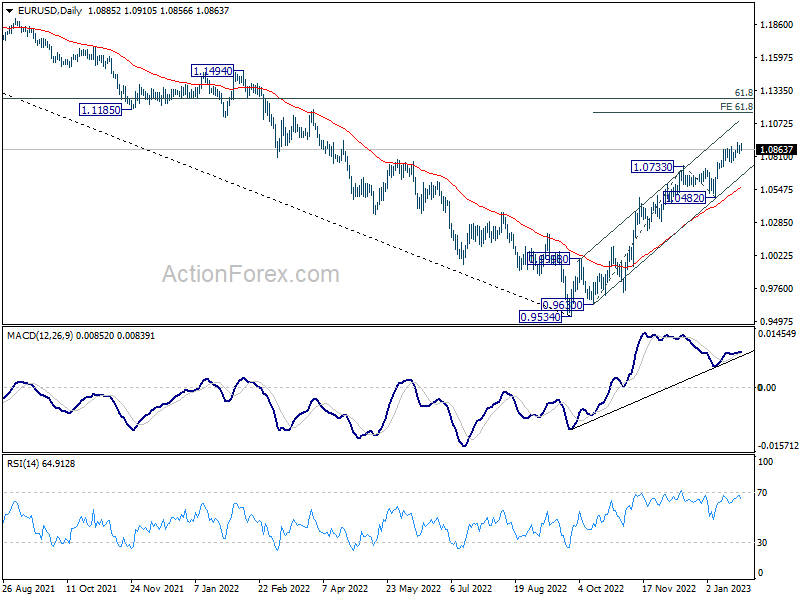

In the bigger picture, current development suggests that the rally from 0.9534 low (2022 low) is a medium term up trend rather than a correction. Further rise is in favor to 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 next. This will remain the favored case as long as 1.0482 support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | CPI Q/Q Q4 | 1.40% | 1.50% | 2.20% | |

| 21:45 | NZD | CPI Y/Y Q4 | 7.20% | 7.10% | 7.20% | |

| 23:30 | AUD | Westpac Leading Index M/M Dec | -0.10% | -0.10% | ||

| 00:30 | AUD | CPI Q/Q Q4 | 1.90% | 1.70% | 1.80% | |

| 00:30 | AUD | CPI Y/Y Q4 | 7.80% | 7.50% | 7.30% | |

| 00:30 | AUD | RBA Trimmed Mean CPI Q/Q Q4 | 1.70% | 1.60% | 1.80% | 1.90% |

| 00:30 | AUD | RBA Trimmed Mean CPI Y/Y Q4 | 6.90% | 6.50% | 6.10% | |

| 00:30 | AUD | Monthly CPI Y/Y Dec | 8.40% | 7.70% | 7.30% | |

| 07:00 | GBP | PPI Input M/M Dec | -1.10% | 0.90% | 0.60% | -0.20% |

| 07:00 | GBP | PPI Input Y/Y Dec | 16.50% | 19.20% | 19.20% | 18.00% |

| 07:00 | GBP | PPI Output M/M Dec | -0.80% | 0.70% | 0.30% | -0.10% |

| 07:00 | GBP | PPI Output Y/Y Dec | 14.70% | 13.90% | 14.80% | 16.20% |

| 07:00 | GBP | PPI Core Output M/M Dec | 0.10% | 1.10% | 0.50% | |

| 07:00 | GBP | PPI Core Output Y/Y Dec | 12.40% | 13.90% | 13.30% | 13.00% |

| 09:00 | CHF | Credit Suisse Economic Expectations Jan | -40 | -42.8 | ||

| 09:00 | EUR | Germany IFO Business Climate Jan | 90.2 | 90.5 | 88.6 | |

| 09:00 | EUR | Germany IFO Current Assessment Jan | 94.1 | 95 | 94.4 | |

| 09:00 | EUR | Germany IFO Expectations Jan | 86.4 | 85 | 83.2 | |

| 15:00 | CAD | BoC Rate Decision | 4.50% | 4.25% | ||

| 15:30 | USD | Crude Oil Inventories | 1.2M | 8.4M | ||

| 16:00 | CAD | BoC Press Conference |