Sterling falls broadly today and poor PMI data indicates that recession is continuing in the UK. Comparatively, Eurozone PMIs argue that it might have escaped recession. For now, the Pound is the worst performer for the day, followed by Swiss Franc, and then Aussie. Yen is the strongest, trying to recover again, followed by Canadian and Dollar. Euro is mixed in between.

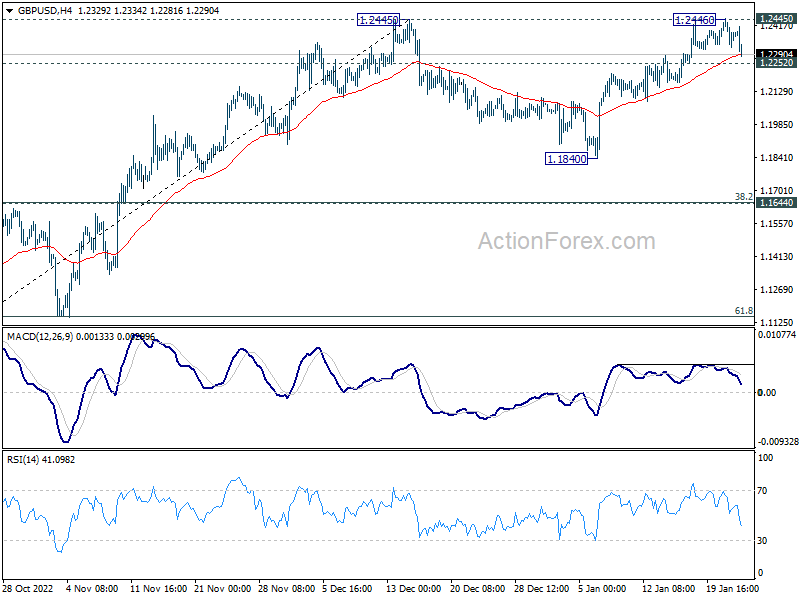

Technically, some attention will be on 1.2252 minor support in GBP/USD for the rest of the day. Break there will indicate that rise from 1.1840 has completed after rejection by 1.2445 resistance. Bias will be back on the downside for 1.1840 support again, as the corrective pattern from 1.2445 starts the third leg. Such development will more likely be accompanied by selloff in the Pound elsewhere, rather than Dollar buying.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.23%. DAX is down -0.23%. CAC is up 0.02%. Germany 10-year yield is down -0.0074 at 2.197. Earlier in Asia, Nikkei rose 1.46. Japan 10-year JGB yield rose 0.0338. Hong Kong, China, and Singapore were still on holidays.

UK PMI composite hit 24-month low, decline rate remains only modest

UK PMI Manufacturing rose from 45.3 to 46.7 in January, above expectation of 45.4. However, PMI Services dropped from 49.9 to 48.0, below expectation of 49.6, hitting a 24-month low. PMI Composite dropped from 49.0 to 47.8, a 24-month low too.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said: “Weaker than expected PMI numbers in January underscore the risk of the UK slipping into recession… There were some bright spots in the survey, including improved business expectations for the year ahead and a further cooling of inflationary pressures. The overall rate of decline indicated also remains only modest. But this is undeniably a disappointing start to the year for the UK.”

Eurozone PMI composite rose to 50.2, escaping recession but renewed contraction shouldn’t be ruled out

Eurozone PMI Manufacturing rose from 47.8 to 48.8 in January, above expectation of 48.1. PMI services rose from 49.8 to 50.7, above expectation of of 49.4, and back in expansion. PMI Composite rose from 49.3 to 50.2, a 7-month high.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

“A steadying of the eurozone economy at the start of the years adds to evidence that the region might escape recession…. The region is by no means out of the woods yet, however, as demand continues to fall – merely dropping at a reduced rate… The case for higher interest rates is fuelled further by the upturn in employment growth recorded during the month and signs of higher wages driving the latest upturn in price pressures.

“A case for policy caution is supported by the survey merely indicating a stagnation of the eurozone economy, hinting that a renewed slide into contraction should not be ruled out as borrowing costs rise, but the survey undoubtedly brings welcome good news to suggest that any downturn is likely to be far less severe than previously feared and that a recession may well be avoided altogether.”

Germany Gfk consumer sentiment rose to -33.9, positive trend consolidating

Germany Gfk consumer sentiment for February rose 3.7 pts to -33.9, below expectation of -33.0. In January, Economic expectations improved from -10.3 to -0.6. Income expectations rose from -43.4 to -32.2. Propensity to buy dropped from -16.3 to -18.7.

“With the fourth increase in a row, the positive trend in consumer sentiment is consolidating. Even though the level is still very low, pessimism has eased recently”, explains GfK consumer expert Rolf Bürkl.

“Falling energy prices, such as for gasoline and heating oil, have ensured that consumer sentiment is less gloomy. Nevertheless, 2023 will remain difficult for the domestic economy. Private consumption will not be able to positively contribute to overall economic development this year. This is also signaled by the still very low level of the indicator.”

Japan PMI manufacturing unchanged at 48.9, services rose to 52.4

Japan PMI Manufacturing was unchanged at 48.9 in January, below expectation of 49.4. PMI Services rose from 51.5 to 52.4. PMI Composite rose form 49.7 to 50.8.

Laura Denman, Economist at S&P Global Market Intelligence, said: “Japan’s private sector kicked off 2023 on a more positive note, as signalled by activity returning to growth territory in January. However, similar to trends recorded over much of the past six months, a divergence between the manufacturing and services sectors has remained.

Australia PMI composite rose to 48.2, economy is not slowing sufficiently for RBA

Australia PMI Manufacturing fell from 50.2 to 49.8 in January, a 32-month low. PMI Services rose from 47.3 to 48.3. PMI Composite rose from 47.5 to 48.2.

Warren Hogan, Chief Economic Advisor at Judo Bank said:

“Following eight consecutive rate hikes in 2022, the RBA Board will be meeting for the first time on 7 February. The latest PMI readings may raise the concern that the economy is not slowing sufficiently to bring inflation back to target in a timely manner…

“Inflation pressures may abate somewhat but the risk for the RBA is that inflation remains stubbornly high well into 2023. This could maintain upward pressure on inflation expectations and wages growth. On this basis it seems premature for the RBA to pause the current tightening cycle….

“We expect the RBA to hike the cash rate by 25bp in each of February and March before an extended pause. Further rate hikes may be required later in 2023 if the economy and inflation prove more resilient than current consensus forecasts suggest.”

Australia NAB business conditions fell to 12, confidence improved to -1

Australia NAB Business Conditions fell from 20 to 12 in December. Trading conditions fell from 27 to 18. Profitability conditions fell from 19 to 12. Employment conditions also declined from 13 to 8. Business Confidence improved from -4 to -1.

NAB Chief Economist Alan Oster said: “The main message from the December monthly survey is that the growth momentum has slowed significantly in late 2022 while price and purchase cost pressures have probably peaked”.

“The gap between current business conditions and business confidence remains wider than usual though has narrowed. Ultimately while on average business reports still healthy activity at present, they don’t necessarily expect that to last.”

NZ BusinessNZ services dropped to 52.1, marked a significant slowdown

New Zealand BusinessNZ Performance of Services Index dropped from 53.8 to 52.1 in December. Looking at some details, activity/sales dropped notably from 58.2 to 52.1. Employment fell from 51.8 to 47.1. New orders/business rose from 57.4 to 58.4. Stocks/inventories declined from 54.6 to 51.7. Supplier deliveries increased from 46.8 to 53.4.

BNZ Senior Economist Craig Ebert said that “December marked a significant slowdown in a short space of time for the PSI, although the maintained loftiness in New Orders/Business suggested there was still a lot of demand-side pressure at play”.

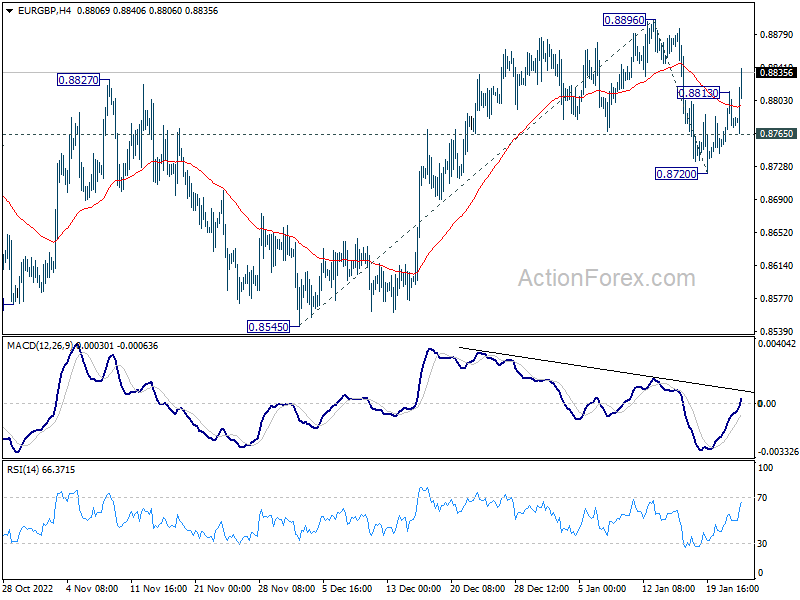

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8752; (P) 0.8784; (R1) 0.8813; More…

EUR/GBP’s rebound from 0.8270 resumed after brief consolidations. Intraday bias is back on the upside for retesting 0.8896 resistance. Firm break there will resume whole rise from 0.8896 to 61.8% projection of 0.8545 to 0.8896 from 0.8720 at 0.8937. On the downside, below 0.8765 minor support will turn intraday bias neutral again.

{kind=link}

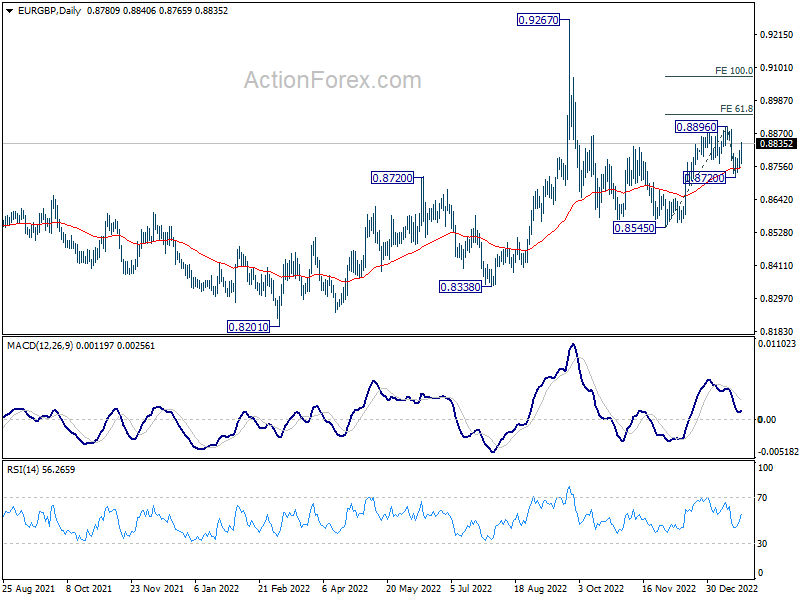

In the bigger picture, the notable support from 55 day EMA (now at 0.8752) retains near term bullishness. Break of 0.8896 should target 0.9267 (2022 high) and possibly above, to resume whole up trend from 0.8201 (2022 low). However, break of 0.8270 support and sustained trading below 55 day EMA will set the stage for 0.8545 and below.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:00 | AUD | Manufacturing PMI Jan P | 49.8 | 50.2 | ||

| 22:00 | AUD | Services PMI Jan P | 48.3 | 47.3 | ||

| 00:30 | AUD | NAB Business Conditions Dec | 12 | 20 | ||

| 00:30 | AUD | NAB Business Confidence Dec | -1 | -4 | ||

| 00:30 | JPY | Manufacturing PMI Jan P | 48.9 | 49.4 | 48.9 | |

| 07:00 | EUR | Germany Gfk Consumer Confidence Feb | -33.9 | -33 | -37.8 | -37.6 |

| 07:00 | CHF | Trade Balance (CHF) Dec | 2.83B | 3.23B | 2.31B | |

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Dec | 26.6B | 20.3B | 21.2B | |

| 08:15 | EUR | France Manufacturing PMI Jan P | 50.8 | 49.6 | 49.2 | |

| 08:15 | EUR | France Services PMI Jan P | 49.2 | 49.7 | 49.5 | |

| 08:30 | EUR | Germany Manufacturing PMI Jan P | 47 | 47.5 | 47.1 | |

| 08:30 | EUR | Germany Services PMI Jan P | 50.4 | 49.6 | 49.2 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Jan P | 48.8 | 48.1 | 47.8 | |

| 09:00 | EUR | Eurozone Services PMI Jan P | 50.7 | 49.4 | 49.8 | |

| 09:30 | GBP | Manufacturing PMI Jan P | 46.7 | 45.4 | 45.3 | |

| 09:30 | GBP | Services PMI Jan P | 48 | 49.6 | 49.9 | |

| 14:45 | USD | Manufacturing PMI Jan P | 46.1 | 46.2 | ||

| 14:45 | USD | Services PMI Jan P | 44.5 | 44.7 |