Canadian Dollar is currently the weakest one in otherwise sluggish markets. Falling oil price is a factor dragging down the Loonie, and traders are also cautious on a dovish rate hike by BoC tomorrow. There is still no clear follow through buying in Dollar against others. Aussie is steady after RBA rate hike earlier today, but looks vulnerable. meanwhile, European majors are mixed with Swiss Franc having a slight upper hand. Yen is apparently waiting for guidance from the stock and bond markets.

Technically, WTI oil’s recovery from 74.10 might have completed at 83.82 already, capped well below 55 day EMA. Retest of 74.10 should be seen rather soon. Firm break there will resume larger down trend to 61.8% projection of 124.12 to 76.61 from 94.25 at 64.88. If happens, that might lift USD/CAD for at least a test on 1.3976 high.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.46%. DAX is down-0.28%. CAC is down -0.22%. Germany 10-year yield is down -0.0757 to 1.807. Earlier in Asia, Nikkei rose 0.24%. Hong Kong HSI dropped -0.40%. China Shanghai SSE rose 0.02%. Singapore Strait Times dropped -0.46%. Japan 10-year JGB yield dropped -0.0052 to 0.253.

US trade deficit widened to USD -78.2B in Oct

US exports of goods and services dropped USD 1.9B over the month in October, while imports rose USD 2.2B. Trade deficit widened from USD -74.1B to USD -78.2B, smaller than expectation of USD -79.4B.

The increased in goods and services trade deficit reflected an increased in goods deficit of USD 6.1B to USD -99.6B, and increased in services surplus of USD 2.1B to USD 21.4B.

ECB Lane reasonably confidence EZ close to peak inflation

ECB Chief Economist Philip Lane said in an interview, “I would be reasonably confident in saying that it is likely we are close to peak inflation”. But it’s still uncertain whether inflation has peaked or it will arrive at the start of 2023. He didn’t rule out some extra inflation early next year. But, “once we are past the initial months of 2023, later on in 2023 – in the spring or summer – we should see a sizeable drop in the inflation rate.” Still, the journey back to 2% will “take time”.

“We need to recognise that the interest rate decisions we have already made will help to reduce the inflation rate next year and the year after that,” he said. “We do expect that more rate increases will be necessary, but a lot has been done already, so we will have to ensure we have a good understanding of the inflation outlook, and the risk factors when setting the interest rate on a meeting-by-meeting basis.”

Lane also said, “QT should essentially be a background programme”. That is, policymakers will ensure QT makes its contribution to policy normalization in “a way that reinforces the primary instrument, which is setting rates”.

ECB Herodotou: There will be another hike or hikes

ECB Governing Council member Constantinos Herodotou said, “We are very near the neutral rate. There will be I think another hike or hikes.”

“There are a number of variables that may give some comfort and should there be an economic impact, it won’t be.. a hard landing” he said, pointing to fiscal support and the robust jobs market.

RBA hikes 25bps, expects to increase interest rates further

RBA raises cash rate by 25bps to 3.10% as widely expected. Tightening bias is maintained as “the Board expects to increase interest rates further over the period ahead”, even though it’s “not on a pre-set course”. The size and timing of future rate hikes will continue to be determined by incoming data and the outlook for inflation and job market. The path to slow inflation and achieve a soft landing remains a “narrow one”.

The central bank expects inflation to peak at around 8% in Q4, and then decline next year due to “ongoing resolution of global supply-side problems, recent declines in some commodity prices and slower growth in demand”. Medium-term inflation expectations “remain well anchored”. Inflation is expected to decline to “a little over 3 per cent over 2024”.

RBA also expects growth to “moderate over the year ahead” to 1.50% in 2023 and 2024. Labor market remains “very tight” but employment growth has slowed. Wages growth is “continuing to pick up”. “Given the importance of avoiding a prices-wages spiral, the Board will continue to pay close attention to both the evolution of labour costs and the price-setting behaviour of firms in the period ahead.”

BoJ Kuroda: Premature to discuss specifics of monetary policy framework

BoJ Governor Haruhiko Kuroda told the parliament, “the BOJ is seeking to sustainably and stably achieve its 2% inflation target accompanied by wage growth. Our view is that this will likely take more time.”

“It’s therefore premature to discuss specifics about our monetary policy framework,” he said.

“We’ll maintain our current monetary policy to make it easier for companies to raise wages,” he added.

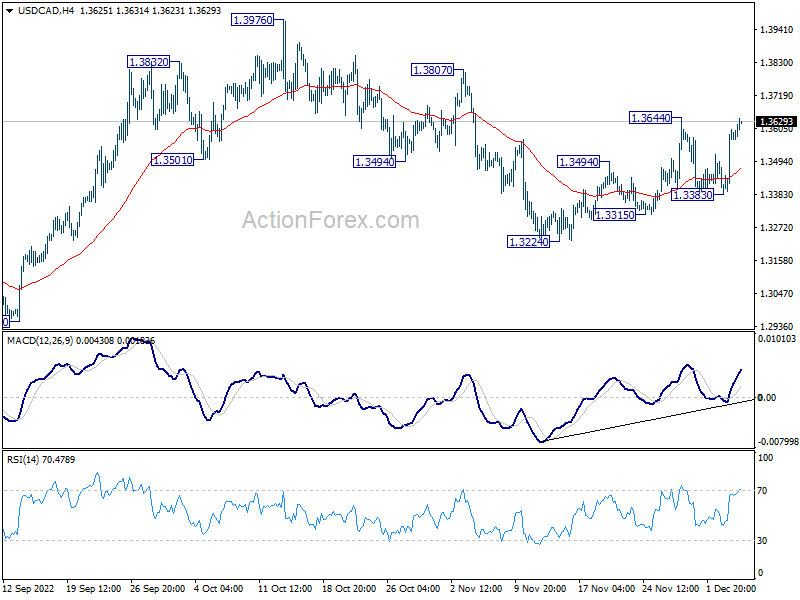

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3447; (P) 1.3526; (R1) 1.3667; More….

Intraday bias in USD/CAD stays neutral first with immediate focus on 1.3644 resistance. Firm break there will affirm the case that correction from 1.3976 has completed at 1.3224. Further rise should then be seen to 1.3807 resistance first. However, break of 1.3383 will likely resume the fall from 1.3976 through 1.3222 cluster support, which carries larger bearish implications.

{kind=link}

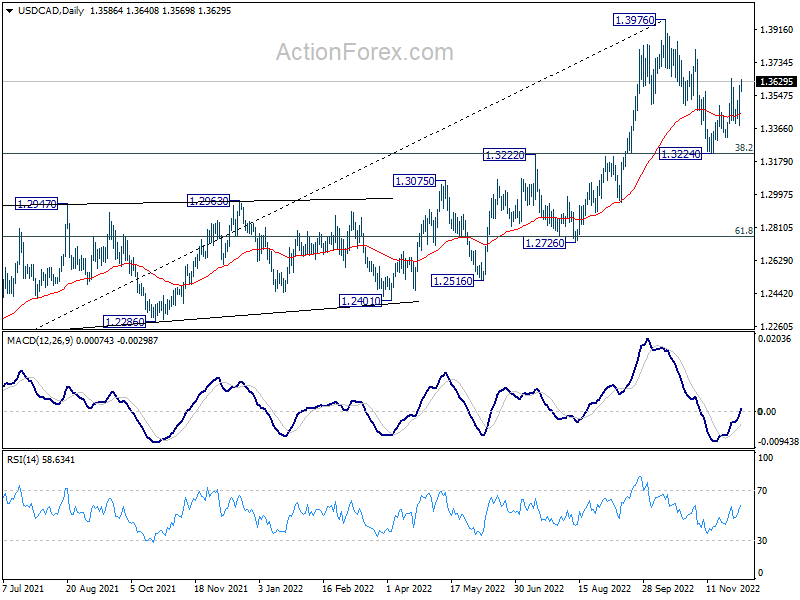

In the bigger picture, as long as 1.3222 cluster support (38.2% retracement of 1.2005 to 1.3976 at 1.3223) holds, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 high at a later stage. However, firm break of 1.3222/3 will indicate that the trend might have reversed. Deeper fall would be seen to next cluster support at 1.2726 (61.8% retracement at 1.2758).

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Oct | 1.80% | 2.00% | 2.10% | 2.20% |

| 23:30 | JPY | Household Spending Y/Y Oct | 1.20% | 0.90% | 2.30% | |

| 00:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Nov | 4.10% | 1.20% | ||

| 00:30 | AUD | Current Account Balance (AUD) Q3 | -2.3B | 6.3B | 18.3B | 14.7B |

| 03:30 | AUD | RBA Interest Rate Decision | 3.10% | 3.10% | 2.85% | |

| 07:00 | EUR | Germany Factory Orders M/M Oct | 0.80% | 0.20% | -4.00% | -2.90% |

| 09:30 | GBP | Construction PMI Nov | 50.4 | 52.7 | 53.2 | |

| 13:30 | CAD | Trade Balance (CAD) Oct | 1.2B | 0.9B | 1.1B | 0.6B |

| 13:30 | USD | Trade Balance (USD) Oct | -78.2B | -79.4B | -73.3B | -74.1B |