Overall risk sentiment is rather indecisive in the markets. While US stocks staged a strong rebound overnight, there is no follow through buying in Asia. Dollar and Yen are trading mildly higher today, together with Swiss Franc. New Zealand Dollar is leading commodity currencies lower. Sterling is mixed for now but more volatility is likely with UK CPI release featured.

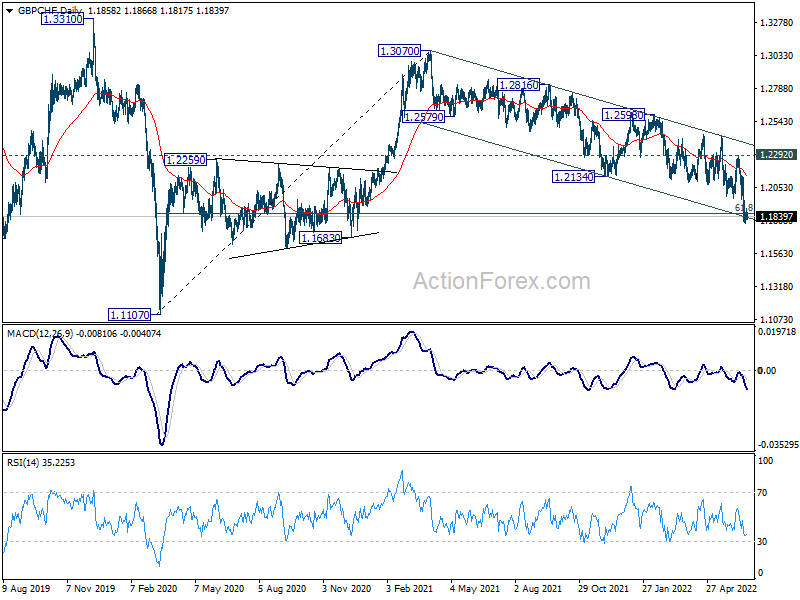

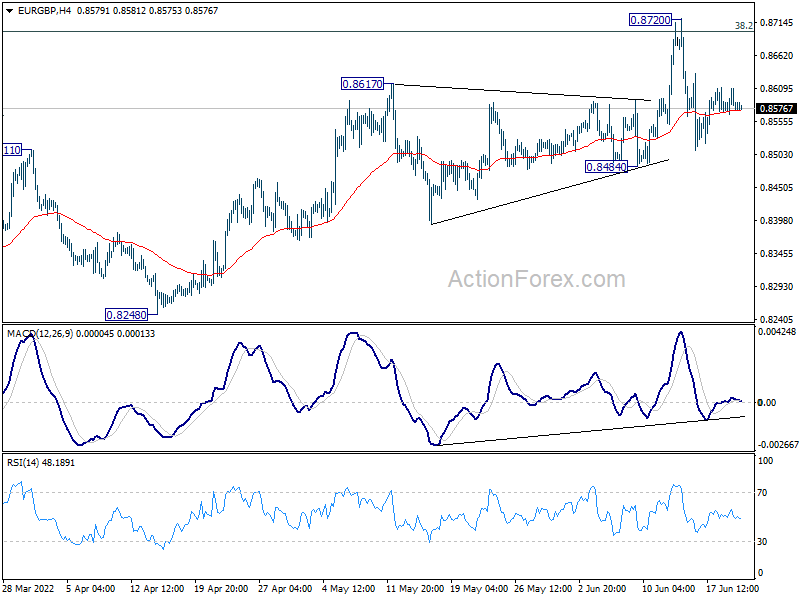

Technically, Sterling is at a juncture against Euro and Swiss. EUR/GBP is pressing medium term fibonacci level of 38.2% retracement of 0.9499 to 0.8201 at 0.8697. GBP/CHF is also pressing 61.8% retracement of 1.1107 to 1.3070 at 1.1857. Sustained break of these levels could prompt even sharper selloff in the Pound. Let’s see.

{kind=link}

In Asia, at the time of writing, Nikkei is down -0.07%. Hong Kong HSI is down -1.19%. China Shanghai SSE is down -0.62%. Singapore Strait Times is down -0.16%. Japan 10-year JGB yield is up 0.0030 at 0.239. Overnight, DOW rose 2.15%. S&P 500 rose 2.45%. NASDAQ rose 2.51%. 10-year yield rose 0.068 to 3.307.

BoJ firm on maintaining ultra-loose monetary policy

In the minutes of April 27-28 meeting of BoJ indicated that while the board was concerned with fluctuation in Yen’s exchanger rate, it remained firm on the stance to continue with ultra-loose monetary policy.

One board member noted that Japan’s economy was “still on its way to recovery”. As a “commodity importer”, the rise in commodity prices would “lead to an outflow of income from Japan and thus exert downward pressure on the economy.” Hence, it’s “necessary” to “continue with the current powerful monetary easing and thereby firmly support the economy.”

Another member noted that “the challenge of monetary policy in Japan was not to curb inflation, as in the case of the United States and Europe, but to overcome inflation that was still too low”. A different member commented that,” with the addition of Russia’s invasion of Ukraine to the existing downside risks to the economy, the situation had further changed significantly; against this backdrop, it was not appropriate for the Bank to make any big changes to its monetary policy stance.”

Regarding Yen’s depreciation, “a few members said excessive fluctuations in the foreign exchange market over a short period of time, such as those observed recently, would raise uncertainties about the future and make it more difficult for firms to formulate their business plans”.

Some member noted, “it was necessary for the Bank to clearly communicate to the public that the aim of monetary policy conduct was to fulfill its mandate of achieving price stability, rather than to control foreign exchange rates.”

Australia Westpac leading index dropped to 0.58 in May

Australia Westpac leading index dropped form 1.09% to 0.58% in May, still indicating above trend growth for 2022. Westpac said, “the components of the Index are indicating an important emerging theme around Australia’s growth prospects – a significant shock to consumer confidence.”

On RBA policy, Westpac expects the central bank to hike a further 50bps in July. It assessed that at 1.35% after the hike, interest rate is still below the neutral setting. Given the tight labor market and rising inflation, further monetary tightening can be expected through 2022.

New Zealand goods exports rose 18% yoy in May, imports rose 24% yoy

New Zealand goods exports rose 18% yoy or NZD 1.1B to NZD 7.0B in May. Goods imports rose 24% yoy or NZD 1.3B to NZD 6.7B. Monthly trade surplus narrowed from NZD 440m to NZD 263m, smaller than expectation of NZD 580m.

Exports to all top destinations rose except to China: China (down -3.8%), Australia (up 49%), US (up 18%), EU (up 23%), Japan (up 0.7%).

Imports from most partners rose except from the US: China (up 25%), EU (up 12%), Australia (up 18%), US (down -5.5%), Japan (up 41%).

Looking ahead

UK CPI and PPI are the main focus in European session. Canada will also release CPI later in the day.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8563; (P) 0.8586; (R1) 0.8605; More…

Intraday bias in EUR/GBP remains neutral and further rise is expected with 0.8484 support intact. On the upside, break of 0.8720 and sustained trading above 0.8697 medium term fibonacci level will carry larger bullish implication. Next target is 0.9003 fibonacci level. However, break of 0.8484 will indicate rejection by 0.8697 and turn near term outlook bearish.

{kind=link}

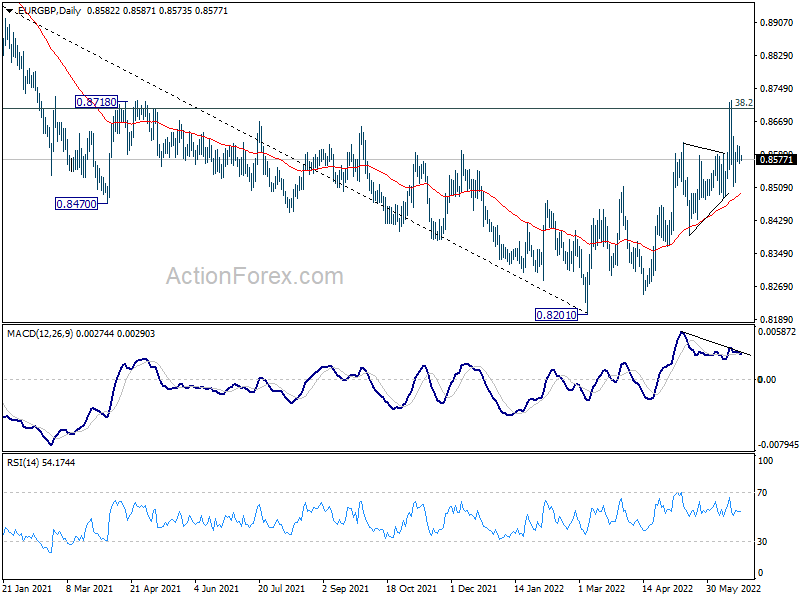

In the bigger picture, rise from 0.8201 medium term bottom could could either be a correction to the down trend from 0.9499 (2020 high), or a medium term up trend itself. Sustained break of 38.2% retracement of 0.9499 to 0.8201 at 0.8697 will affirm the latter case, and pave the way to 61.8% retracement at 0.9003. However, rejection by 0.8697 will maintain medium term bearishness.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) May | 263M | 580M | 584M | 440M |

| 23:50 | JPY | BoJ Meeting Minutes | ||||

| 00:30 | AUD | Westpac Leading Index M/M May | -0.10% | -0.10% | ||

| 06:00 | GBP | CPI M/M May | 1.90% | 2.50% | ||

| 06:00 | GBP | CPI Y/Y May | 9.10% | 9.00% | ||

| 06:00 | GBP | Core CPI Y/Y May | 6.00% | 6.20% | ||

| 06:00 | GBP | RPI M/M May | 0.40% | 3.40% | ||

| 06:00 | GBP | RPI Y/Y May | 11.30% | 11.10% | ||

| 06:00 | GBP | PPI Input M/M May | 0.70% | 1.10% | ||

| 06:00 | GBP | PPI Input Y/Y May | 19.90% | 18.60% | ||

| 06:00 | GBP | PPI Output M/M May | 1.80% | 2.30% | ||

| 06:00 | GBP | PPI Output Y/Y May | 15% | 14% | ||

| 06:00 | GBP | PPI Core Output M/M May | 2.00% | 1.60% | ||

| 06:00 | GBP | PPI Core Output Y/Y May | 13.70% | 13.00% | ||

| 12:30 | CAD | CPI M/M May | 0.90% | 0.60% | ||

| 12:30 | CAD | CPI Y/Y May | 7.50% | 6.80% | ||

| 12:30 | CAD | CPI Common Y/Y May | 3.40% | 3.20% | ||

| 12:30 | CAD | CPI Median Y/Y May | 4.70% | 4.40% | ||

| 12:30 | CAD | CPI Trimmed Y/Y May | 5.40% | 5.10% | ||

| 14:00 | EUR | Eurozone Consumer Confidence Jun P | -20 | -21 |